Take Advantage of IRS Section 179 Before the End of 2020

- December 28, 2020

- 12:28 pm

- Section 179, Taxes

As 2020 draws to a close, businesses all over the world are taking the time to reflect on the turbulent year, are making any last-minute changes to their plans, and are deciding the basis of the coming year’s procedures.

One thing you should start considering if you haven’t before this point is taking advantage of the IRS Section 179 tax deductions. This law gives you an incredibly affordable opportunity to finance your equipment upgrades or any other renovations you may have been planning.

The deadline to benefit from this is fast approaching though and the sooner you understand Section 179, the sooner you can make the best possible long-term decision for your business.

IRS Section 179 Explained

In a nutshell, Section 179 of the IRS tax code is an incentive formulated by the US Government that is specifically designed to encourage small businesses to increase their spending. This spending could be in the form of upgrading existing equipment as an example or implementing a new industrial workflow through updated machinery.

Section 179 does this by deducting the full purchase price of qualifying equipment or software bought during the tax year. This would allow companies to deduct the full price from their gross income as this expense would be considered a tax write off.

Specifics You Need to Know

To take advantage of this, the equipment you’re looking to purchase has to be eligible, and said equipment has to be bought and put to use BEFORE midnight on December 31st, 2020. There are also spending caps in place, mainly a:

- $1,040,000 deduction limit

- $2,590,000 spending cap.

The equipment you’re financing has to fall in one of the following categories to be eligible for Section 179:

Eligible for Section 179

- Hardware (machinery, robots, computers, etc.)

- Furniture

- Vehicles designed for commercial usage (shuttle vans, cargo vans, trailers, etc.)

- Off the shelf software

- Property that is not a part of the building’s structure

- Certain non-residential building renovations (roofing, alarms, fire systems, etc.)

Unfortunately, you cannot at this point in time take advantage of Section 179 tax deductions if your planned equipment upgrade falls into the following categories:

Ineligible

- Property (permanent buildings, structures, swimming pools, parking areas, etc.)

- Property being used or upgraded outside the US

- Property used for the purpose of furnishing lodging

- Property inherited or taken as a gift

- Any property that does not fall into the category of personal property

The Benefits for Your Business

As Section 179 was passed in the hopes of bolstering general economic activity, it’s no surprise that many businesses will find the law quite helpful. A problem that plagues companies, especially the ones that operate at a smaller scale, is finding the resources to upgrade or automate their production processes and software.

These upgrades are very rarely affordable which is why many businesses have to continue to use older, unreliable equipment to carry out their production in the hopes of keeping their overall spending and costs down. This law changes all this. The IRS Section 179 tax deductions help alleviate a lot of the burden business owners face when making these tough decisions. Potential upgrades that may have been in the pipeline for years, can finally become a reality.

Better equipment will allow businesses to produce more products at a better quality and a lower price. It might also allow them to try newer, more innovative production methods to give their consumers an incredible product that helps their bottom-line and develops brand loyalty. All these factors play a big part in achieving economies of scale; a goal most businesses are actively striving towards achieving.

Next Steps

Now that you know all about the IRS Section 179 tax deductions, it’s time to understand the next steps on what you have to do.

The most important thing is making sure your upgrade is eligible and then acknowledging the December 31st deadline we’ve outlined before. As the month is almost drawing to a close, time is short and you will have to act fast if you’re still interested in your business benefiting from this law for 2020.

To claim the Section 179 deduction, you have to specify this on Part 1 of Form 4562. Include a description of the property, its cost, and the overall amount of Section 179 you’re claiming on this asset on Line 6. A list might also be attached in case you need more room.

If you’re unwilling or unqualified to fill this out, then it’s probably a good idea to hire an accountant to do this for you.

In terms of gathering funds, you can choose any financing option for your equipment upgrades and the Section 179 deduction would comply with almost all of them. This includes private financing companies like Dimension Funding. Choosing to finance your industrial automation upgrade through private financing companies like Dimension Funding has a myriad of benefits that banks and other lenders simply can’t provide.

Recent Posts

- Bonus Depreciation is About to Phase Down to 80% in 2023 December 29, 2022

- Tax Benefits of Buying Equipment & Software Before December 31, 2022 December 8, 2022

- How the Inflation Reduction Act Impacts your Business and You and your Family August 16, 2022

- Recession? What Recession? July 27, 2022

- Dimension Funding Has Paperless Financing April 26, 2022

One benefit that comes with equipment financing over bank financing the bank requires a “Blanket Lien” meaning that all of assets of the company are security for the financed equipment. With a financing company, the financing is unsecured with only the equipment as security.

One benefit that comes with equipment financing over bank financing the bank requires a “Blanket Lien” meaning that all of assets of the company are security for the financed equipment. With a financing company, the financing is unsecured with only the equipment as security. The tax benefits of financing your equipment purchases should also be something business owners take into consideration when deciding on financing equipment. When you make financing payments, you are paying on the interest in addition to the amount applied towards the purchase price of the equipment. The interest payment portion of your loan is tax deductible each year that you are paying on the loan.

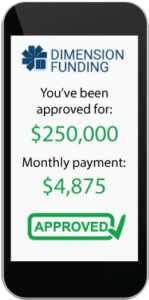

The tax benefits of financing your equipment purchases should also be something business owners take into consideration when deciding on financing equipment. When you make financing payments, you are paying on the interest in addition to the amount applied towards the purchase price of the equipment. The interest payment portion of your loan is tax deductible each year that you are paying on the loan. Applying for these loans are easy and simple. You can apply for up to $250k without providing financial statements and if you need more than that, the paperwork process is streamlined for your convenience. When you

Applying for these loans are easy and simple. You can apply for up to $250k without providing financial statements and if you need more than that, the paperwork process is streamlined for your convenience. When you